Latest News

The road to Brexit: a dash for the exit, but beware the ‘cliff-edge’ beyond

13th December 2019

A way out of the Brexit impasse

The political and constitutional deadlock of the past year has finally been resolved, with the Conservative Party gaining a substantial majority at the General Election. Boris Johnson will therefore enjoy a more favourable position in the House of Commons than any Prime Minister since Tony Blair after the 2001 election. The new Parliament will assemble on Tuesday, with the Government led by Boris Johnson now facing no parliamentary obstacles to prevent the UK’s formal departure from the EU at the end of January. But there’s still a cliff-edge to worry about, albeit one of a slightly different nature, and this will cloud the economic prospects for the UK until it is resolved.

With the electorate having delivered a clear verdict at Thursday’s election, the scene is now set for rapid progress on completing the formalities of the Brexit process. The EU Withdrawal and Implementation Bill, which was originally introduced into the House of Commons in October, is expected to be re-presented before Christmas, possibly on 20th December. There will now be nothing that opposition parties can do to thwart its speedy progress through the Commons and, with the Conservatives having laid out their approach to Brexit clearly in their manifesto, the House of Lords will not stand in its way. There will need to be a fourth, and final, ‘meaningful vote’ on the Withdrawal Agreement and the associated Political Declaration, but this will now be a formality.

Feeling better, but the economic numbers won’t show it

The lifting of ‘Brexit uncertainty’ will lead to a collective sigh of relief and provide an immediate boost to confidence across the economy. The past three years have seen the economy meandering along in an increasingly anaemic state of health. From 2016 to 2018 the culprit was the currency shock to the economy as the depreciation of sterling pushed up inflation and squeezed the spending power of households. That initial impact has worn off, but over the past year has been replaced by a general lack of confidence as businesses and consumers have been unwilling to take on commitments against the risk of a ‘no deal’ exit.

Indeed, figures released by the Office for National Statistics (ONS) on 10th December showed that economic activity has flat-lined since July, with the Purchasing Managers’ surveys for November pointing to a contraction of activity. It’s therefore quite possible that GDP will contract in the final quarter, with the growth rate for 2019 set to come in at only a little over 1%.

Normal service is resumed

With politics no longer providing daily high-octane drama most people will be pleased to get back to their normal lives and put the saga of Brexit behind them. A bounce in consumer sentiment, leading to higher spending by households, can therefore be expected in the coming months. After all, the fundamentals of household finances are in much better shape than they were a year or two ago: the annual rate of inflation currently stands at a very muted 1.5%, compared with the peak of 3.1% reached towards the end of 2017, while growth of average earnings stands at around 3.5%. With Brexit worries fading into the background, consumers will be more willing to contemplate ‘big ticket’ purchases and commitments, which will be reflected in a revival of interest in buying houses and cars, and investing in home improvements. It’s likely to be a similar story among businesses, with many firms having put off investment decisions during the past three years.

It should be noted, however, that the positive impact on sentiment will be offset by other factors. To begin with, the prospect of a ‘no deal’ exit during 2019 has left many firms sitting on elevated levels of inventories. In the months leading up to the original 29 March deadline, warehouses were crammed to the rafters; some de-stocking then took place during the pause that followed, only for stocks to be built up again in the run-up to the 31 October deadline. Businesses will now be keen to reduce inventories back to normal levels, which will also help to restore their cashflow positions. But while this process is underway, orders for new stock will be scaled back, leading to lower domestic production and imports. The unwinding of stocks contributed to a small contraction in GDP during the second quarter of this year, and may well do so again in the early months of next year as the process is repeated.

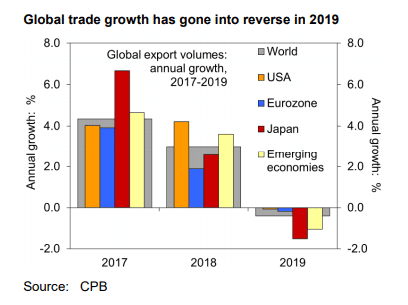

A second reason for caution about the economic prospects for 2020 is the dismal state of the global economy. The trade dispute between America and China remains unresolved, with a wider impact that has weighed on global business sentiment and investment: as a consequence, cross-border trade in goods around the world will be slightly lower this year than it was in 2018 – the first annual decline since 2009. Market conditions for many exporters will therefore be pretty tough, with matters not being helped by the prospect of a further uptick in the value of sterling (of which more later). So, for all that UK consumers may feel more confident during 2020, and more willing to spend, overall it’s set to be a fourth anaemic year, with HSBC forecasting that Britain’s economy will grow by just 1.0%, pretty much in line with the expected outcome for this year.

Not quite the end of the road …

In any case, the respite from Brexit noise might turn out to be short lived. The UK’s formal exit from the EU is only the first stage in a much longer process of fashioning a new economic relationship. On leaving the EU at the end of January, the UK will enter an ‘Implementation Period’ which runs until the end of 2020. The purpose of the Implementation Period is to allow time for the two sides to negotiate the Free Trade Agreement (FTA) which will apply once the UK has completely extricated itself from the EU. During the Implementation Period, little will change: goods and people will still move freely to and from the EU-27; motorists taking their cars across the Channel won’t require additional permits; children going off on school skiing trips in February will still be covered by the EHIC health insurance cards; pets can still travel on their passports. The UK will be free to open negotiations with other countries about trade deals, but they cannot be implemented.

There is also an option for a single extension to the Implementation Period, of either one or two years, with the UK Government required to notify the EU of its intentions at the start of July. Boris Johnson has said on numerous occasions that he will not seek any extension. This is understandable from the perspective of the Government’s desire to press ahead with concluding and implementing trade agreements with non-EU countries. But it also raises the question of what happens if no extension is sought and no trade deal has been agreed. In that eventuality the UK’s trade with the EU would revert to World Trade Organization (WTO) terms, with all that would entail for border processes and tariffs. It would, in effect, be a partial version of the ‘no-deal’ Brexit that businesses have been so keen to avoid, and it would trigger an adverse economic shock to the UK’s economy. Should the negotiations seem to be heading in that direction, it’s likely that business and consumers would start to experience renewed

nervousness in the autumn, ahead of the transition to WTO terms at the start of 2021.

Negotiators from both sides will get down to intensive discussions about a UK-EU trade agreement early in the new year. The ‘Political Declaration’ which accompanies the Withdrawal Agreement makes it clear that Britain is not looking to maintain a customs union with the EU, nor to participate in large swathes of the Single Market. Instead, the aim is to model the new relationship on the FTAs that the EU has negotiated in recent years with Canada, Japan, and South Korea. These FTAs eliminate tariffs and quotas on trade in most goods; they also open up some aspects of trade in services, such as government procurement, shipping, telecommunications, air transport, data transfers and storage; and they also contain provisions for environmental standards and employment rights. But they are a far cry from the existing Single Market relationship, and will introduce some frictions into cross-border trade, investment, and the movement of people. When it comes to moving goods, for instance, there will probably be no tariffs, but exports from the UK will be subject to the EU’s inspection processes, which can be quite onerous in some sectors such as food and animal products.

But reaching agreement on what is often described as a ‘Canada-style’ trade deal may prove impossible in the short time that is available. The negotiators may have to scale back their ambitions, with a ‘bare bones’ agreement having to suffice until a better one can be put in place; and the ‘Canada-plus’ deal that has been envisaged could end up being a ‘Canada-minus’ deal when it takes effect in 2021. It is possible though, that with the election over and the electoral threat from the Brexit Party having been repulsed, the Government might change its stance, and perhaps seek to extend the Implementation Period to allow trade negotiations to continue beyond the end of 2020. Businesses and financial markets will be keenly watching for any such hints in the days and weeks ahead. The risk of a ‘cliff edge’ transition to WTO rules at the end of 2020 is the key risk for the UK next year, but it is one that could be mitigated should the UK Government choose to do so.

The sterling surge

One immediate consequence of the victory of the Conservatives at the General Election has been the strengthening of sterling, which rose to around $1.35 as the votes were being counted. Currency markets will now price sterling on the basis of an orderly exit from the EU, and in the knowledge that the Prime Minister has a sufficiently large majority to allow him to be flexible in the negotiations with the EU. HSBC has long held the view that an orderly departure would push the pound up to $1.45, or around €1.30, as the ‘Brexit discount’ that has weighed on the currency since 2016 is removed. But this process won’t happen overnight, and could be subject to reversals during next year if worries emerge about the potential for a ‘cliff edge’ shift to trading with the EU on WTO terms. But assuming that this outcome is avoided, HSBC expects sterling to reach $1.45 by the end of 2020. British exporters will therefore have to get used to a stronger exchange rate for the foreseeable future.

There could still be a small hangover from Brexit weighing on sterling, especially if it looks like the new trade relationship is going to be based on an unambitious ‘Canada-minus’ type of deal; but this is unlikely to amount to more than a few cents. In other words – and provided of course that the trade negotiations aren’t heading for a dead-end and a WTO outcome – the days of sterling trading at $1.20-1.30 are over.

One of the first tasks of the new Government will be to appoint Mark Carney’s replacement as Governor of the Bank of England, with his successor taking up the post on 1st February. The new Governor and the Monetary Policy Committee will face a tricky choice as to whether interest rates should be trimmed further in order to provide support to what will continue to be a sluggish economy. The Government is likely to announce a package of fiscal stimulus measures when Sajid Javid presents his first Budget, probably in early February. But the sums involved are likely to be fairly small, relative to what was announced in September’s Spending Review. With the budget deficit expected to expand only slowly from just under 2% in the present fiscal year to around 3% in 2023/24, this will provide only the gentlest of fillips to growth.

Bearing all this in mind, HSBC now expects that the Bank of England will opt for one rate cut of 25 basis points during the course of 2020, with the favoured date being in early May. This will take UK Bank Rate back down to 0.5%, and will chime with the approach taken by other central banks against the backdrop of a global economic downturn. Whether one rate cut will make any tangible difference is debatable, but it will at least signal that the Bank of England is willing to lend a hand should the need arise.

Mark Berrisford-Smith

Head of Economics, Commercial Banking

HSBC UK