Latest News

What would Mrs Thatcher think? Rishi Sunak’s first Budget

13th March 2020

Economic commentary

This year will be a big one for fiscal statements. Last year’s Budget, originally scheduled for early December, was postponed because of the General Election. This means that there will be two Budgets in 2020, as well as a Comprehensive Spending Review (CSR), the results of which will be announced in July.

This week’s Budget should have provided the opportunity for the new Conservative administration to set out its economic and fiscal vision for the remainder of this Parliament. But preparations were disrupted in February by the sudden resignation of Sajid Javid, and it has subsequently become apparent that the Government must also respond to the outbreak of COVID-19 in the UK. Some of the big decisions that this Government will need to take, for example about a new fiscal framework about funding for social care, have been put off to another day. But after the short-term measures to mitigate the coronavirus had been dealt with, Rishi Sunak spent most of his hour-long statement setting out the broad parameters for the upcoming spending review and announcing some specific spending measures, especially those related to the Conservative Party’s election manifesto.

With the COVID-19 situation developing rapidly during the past few weeks, some of the measures announced in the Budget are not reflected in either the economic and fiscal forecasts made by the independent Office for Budget Responsibility (OBR) nor in the table of ‘policy measures’, along their costings, which accompany the Budget statement. The Budget’s arithmetic will therefore be subject to considerable revision when the next Budget is presented in the autumn.

Mitigating COVID-19

While the number of coronavirus cases in the UK is still only in the hundreds and the number of deaths in single figures, the outbreak is spreading rapidly across western Europe and the United States. Most major advanced economies will therefore suffer an economic downturn in the coming months. Its severity will depend on the success, or otherwise, of individual governments in tackling the outbreak, and the extent to which normal life is disrupted. But no country will be immune, and given the weakness of growth rates during the present global downturn, most advanced economies are in for a brief (we hope) period of recession.

The Budget has earmarked around £12 billion for measures to reduce the impact on individuals and businesses, especially smaller businesses. This means that the stimulus of nearly £18 billion planned for the 2020/21 fiscal year will end up being closer to £30 billion. These Budget measures, moreover, followed hard on the heels of the Bank of England’s package of monetary easing, aimed at sustaining confidence and improving the flow of finance to SMEs: UK Bank Rate was cut by half a percentage point, the Term Finance Scheme was resurrected, and the countercyclical buffers which commercial banks are required to hold were cut from 1% of eligible capital to zero.

The cornerstone of the Government’s measures is a COVID-19 recovery fund, initially set at £5 billion, which will be used to alleviate pressures on the NHS and on social care. The eligibility rules for Statutory Sick Pay have been relaxed, and employers with fewer than 250 staff will be able to reclaim the cost of two weeks’ sick pay from the government. It will also be made easier for the self-employed and those on low pay to access welfare benefits.

Many small businesses in the retail sector were already due to benefit from a relief of 50% on their business rates in the coming financial year. This relief has been increased to 100%, and will cover some 900,000 properties, and is also extended to cover small businesses in the leisure and hospitality sector. In similar vein, the rebate available to small pubs will be increased from £1,000 to £5,000. Those businesses which already pay little or no business rates will be eligible for grant funding via local authorities of £3,000, a measure which is costed at £2.2 billion. Finally, an additional £1 billion of funding will be made available via the British Business Bank in the form of a COVID-19 Business Interruption Loan Scheme, which will offer finance of up to £1.2 million per business, with the government guaranteeing 80% of the loan.

The return of ‘big government’

With the Conservatives having won last December’s General Election thanks largely to the votes of former Labour supporters in towns across northern England and the midlands, the Government recognizes that this is payback time. Mr Sunak proudly proclaimed that the Conservatives are now the “party of public services”, as he unveiled the largest increase in public expenditure for a generation. After a decade of austerity, the numbers are strikingly large, with most of it being funded by additional borrowing. The Conservatives still claim to be a party of low taxes, but they no longer claim to be a party of low spending. One wonders what Mrs Thatcher would make of it all. The days of rolling back the state are gone: ‘big government’ is back with a vengeance, and by 2022/23 the government’s annual total managed expenditure (TME) will amount to a trillion pounds.

By the reckoning of the OBR, what the Government now proposes is the largest sustained fiscal expansion since that announced in the pre-election Budget of March 1992. As it turned out, much of that expansion was speedily reversed after Britain’s unforeseen exit (‘crashing out’) from the Exchange Rate Mechanism in September of that year.

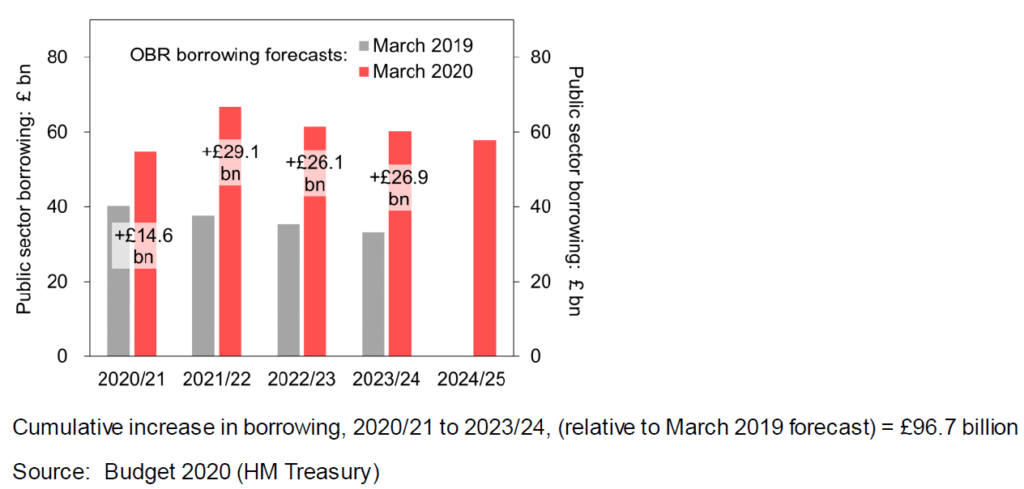

A substantial increase in government borrowing, compared to the 2019 forecast

After a decade of grinding down the government’s annual deficit from around 10% of GDP to just under 2%, this figure is now set climb back above 2%: averaged over the forecasting period to 2024/25, borrowing is expected to be 2.4% of GDP, an increase of 0.8 percentage points compared to the previous forecast. This will push up the level of the national debt by a further £125 billion. This Budget therefore marks a clear reversal of the period of austerity that was set in motion by the coalition government back in 2010. The reversal was arguably begun by the previous administration, in particular in Philip Hammond’s final Budget of October 2018 which announced a large increase in funding for the NHS. Now, in these latest plans, the reduction in real current spending per head of population will have been entirely reversed, by the end of 2024/25.

Given the scale of the stimulus, it’s perhaps surprising that the Government’s fiscal rules are still met. But anybody who has followed Budgets over the years will know that these rules are only ever a fig leaf which Chancellors use to justify their plans. Fiscal rules are almost always met, and if it looks as if they won’t be, then they get changed.

Mr Sunak is working to a loosened set of rules announced by Sajid Javid and reiterated in the recent Queen’s Speech. The Government is required to reach a balanced position on its current budget by 2022/23. It does this, and by a margin of almost £12 billion. It also meets its commitment that net capital expenditure should not exceed 3% of GDP. This is markedly higher than any government has run in several decades, and is key to the Government’s commitment to ‘levelling up’ across the regions.

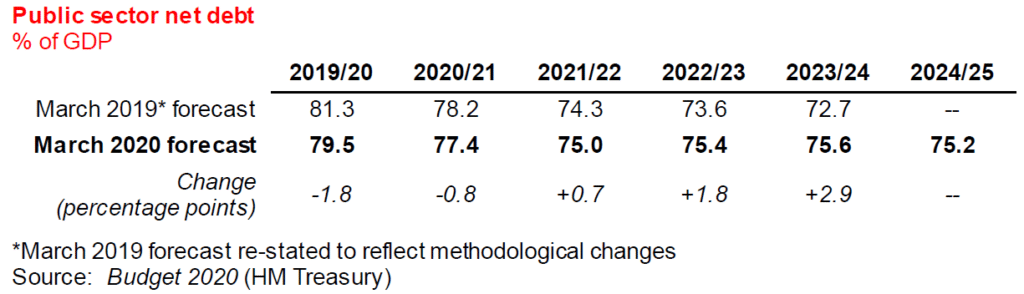

Before the impact of the coronavirus is accounted for, the annual budget deficit, what is termed “public sector net borrowing”, is expected to increase from a projected £47.4 billion in the fiscal year which is just about to end to reach £66.7 billion in 2021/22. As a percentage of GDP, the deficit rises from 1.8% of GDP, peaks at 2.8%, but then falls back to 2.2% in 2024/25. Despite taking on extra borrowing, the ratio of outstanding debt to GDP is expected to fall gradually from 79% to 75% over the forecasting horizon. Nonetheless, if the OBR’s forecasts are correct then 2024/25 will mark the point at which the UK’s national debt, in cash terms, tops two trillion pounds.

Making the sums add up is helped by the very low cost of borrowing money, and by the windfall of no longer having to make contributions to the EU or to send money collected from customs duties to Brussels. Despite running a larger annual deficit, the OBR projects that the ratio of debt interest to receipts will fall from just over 4% today to under 3% in 2024/25. Meanwhile, the Brexit windfall is forecast to total £42.3 billion over the next five fiscal years.

This may be Mr Sunak’s first Budget, but he has quickly learnt the art of budgetary smoke and mirrors. He boasted that the government will spend £640 billion on infrastructure investment during this Parliament; and it’s true that the cumulative total for gross public sector net investment spending out to 2024/25 is, indeed, £640 billion. But the bulk of this isn’t new money. Had Mr Sunak simply confined himself to dealing with the coronavirus outbreak and said nothing at all about public sector investment, the total spent would still amount to around £560 billion.

Over the six years from 2019/20 to 2024/25, the measures in this Budget, together with announcements made in Sajid Javid’s spending statement last September, are reckoned to cost an eye-popping £203.7 billion. A range of tax measures are slated to bring in an extra £28.3 billion over this period, which leaves £175.3 billion to be funded from additional borrowing. Despite the focus on boosting infrastructure spending, about 60% of the extra outlays will be on current (day to day) spending, with capital expenditure accounting for only around 40%.

Certainly, some of the sums earmarked for capital expenditure look impressive when gauged against the thin gruel of recent years. The items grouped together under the heading of “levelling up and getting Britain building” are allocated £90 billion over the years to 2024/25, within which is £21.9 billion that will be spent on fulfilling the Government’s pre-election promises on transport, education, justice, and R&D.

The tax giveaways are less striking, the biggest by far being the increase, to a level of £9,500, in the threshold at which National Insurance Contributions are paid. This measure will take effect from next month, and over the period out to 2024/25 will cost the Exchequer £11.4 billion. Meanwhile, the biggest clawback is the announcement that the rate of Corporation Tax will be maintained at 19%, as opposed to the planned reduction to 17%. Over the forecasting horizon this will boost government coffers by £32.9 billion. As expected, the Chancellor also announced that Entrepreneurs’ Relief on Capital Gains Tax will be scaled back sharply, which will net £6.3 billion, and a big reduction in the availability of relief on ‘red diesel’ which will benefit the Treasury to the tune of £4.9 billion.

Prepared for a shock

The coronavirus epidemic clearly presents considerable risks to the budget arithmetic. It’s possible that not all of the money that has been allocated will be spent, but it’s equally possible that much more could be needed.

The economic forecasts which underpin the Chancellor’s sums could also prove to be over-optimistic. That said, the OBR’s assessment is quite cautious, with their pre-virus forecast for this year being an increase in GDP of 1.1%. Their forecast of an acceleration to 1.8% growth in 2021 is some way above the assessment of the Bank of England (and of HSBC), but thereafter annual growth is assumed to trundle along at 1.5% or a little less. These projections assume a modest improvement in productivity, which may or may not materialize, and could also be thrown off course if the Government’s new immigration policy disrupts the supply of labour.

Above all, it must be hoped that the outbreak of COVID-19 doesn’t cause long-term damage to the economy’s supply capacity. The key objective of the measures taken by the Government and the Bank of England is to ensure, as far as possible, that all sound businesses can withstand the shock (albeit, we hope, a temporary shock) that is to come.

Mark Berrisford-Smith

Head of Economics, Commercial Banking

HSBC UK