Latest News

Contraction in activity remains modest in January

18th February 2025

- Firms retain positive outlook despite sustained drop in activity

- Backlogs depleted at strongest rate for nearly a year

- Output expected to rise across the private sector through 2025

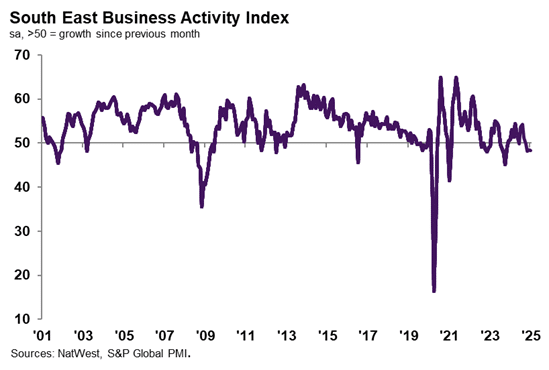

The headline South East Business Activity Index – a seasonally adjusted index that measures the month-on-month change in the combined output of the region’s manufacturing and service sectors – posted at 48.2 in January, down slightly from 48.4 at the end 2024. Although the reading was indicative of reduced private sector output, the rate of decrease was only modest in nature and largely unchanged from that seen in the previous two months.

Private sector firms across the South East continued to make noticeable cuts to their workforce levels at the start of 2025, stretching the current trend of job shedding to five months. Although marked, the rate of reduction eased on the month. Some firms reportedly lowered headcounts as part of cost cutting initiatives and ahead of the National Insurance increase. Others noted difficulties in finding skilled staff.

Nevertheless, South East private sector companies made greater inroads to their backlogged orders in January. Survey respondents linked the decrease to subdued incoming new work and resolved stock issues.

Private sector firms across the South East looked towards the next 12 months with optimism, with the respective index firmly above the crucial 50.0 mark in January. New product launches and growth forecasts linked to strong pipelines and increased marketing efforts were reasons for positive sentiment. The degree of optimism did however dip to its lowest for over two years during the latest survey period.

Catherine van Weenen, Territory Head of Commercial Mid Market at NatWest, said: “The trajectory of the South East private sector remained little changed entering the new year, as declines in activity and new business remained only modest. Encouragingly, the region looked to the future with greater optimism than on average across the UK. South East firms’ increasing ability to finalise orders amid a sustained period of workforce reduction could also reflect some productivity gains.

“The region was not alone in experiencing noticeable cost pressures in January, as input price inflation came in level with the UK average. Seeking to protect margins, firms passed on raised costs to their clients in the form of hiked charges, reflecting some confidence in demand conditions.

“The Bank of England’s interest rate cut last week means that policy is now less restrictive, with further loosening expected in the year ahead.”

The headline figure is the Business Activity Index, calculated from a single question that asks for changes in the volume of business activity compared with one month previously. It is a diffusion index, which is the sum of the percentage of ‘higher’ responses and half the

percentage of ‘unchanged’ responses. It varies between 0 and 100, with a reading above 50 indicating an overall increase in compared to the previous month, and below 50 an overall decrease. The higher above 50, the faster the rate of growth signalled.

Regional profile: South East

Location quotients (see pg 6) can be used to identify clusters of certain types of services and manufacturing businesses – providing unique insight into life and work in that local area.

South East manufacturers are concentrated in:

- Electrical & Optical;

- Mechanical Engineering; and

- Chemicals and plastics.

Services businesses are concentrated in:

- Computing & IT services;

- Transport & communication;

- B2B services.

Performance in relation to UK

South East companies expressed greater confidence than seen on average across the UK. Of the 12 monitored UK areas, Yorkshire & Humber, the West Midlands and Northern Ireland all posted faster contractions in activity than seen locally in January.

Adjusted for seasonal factors, the New Business Index remained below the 50.0 no-change mark in January, to signal a third drop in new orders placed at South East firms in consecutive months. Panellists linked the reduction to a slowdown in demand, often related to raised economic uncertainty.

South East firms signalled a rate of job shedding similar to the UK average (45.3) in January. Backlogs were reduced at a pace exceeding the national trend in the latest survey period.

Reflective of increased wage pressures and higher raw material costs, operating expenses at South East firms rose at a sharper rate in January. In fact, inflation was its strongest for one-and-a-half years. Though robust, local cost pressures were exactly in line with the average seen across the UK.

Meanwhile, the pass through of increased costs to customers was seen by a pick-up in output charges during January. The rate of selling price inflation was substantial, its most pronounced for just over a year and largely in line with national average. Though panellists often blamed increased cost burdens, others reportedly inflated fees ahead of the upcoming UK Minimum Wage increase.

Report here: 110225_RGT_Report_SouthEast.pdf